Cash Freedom Model: Replace Budgeting with Family Harmony

January 16, 2026 - Traditional budgeting sounds great—until you try to live with it. One partner wants spreadsheets, the other wants simplicity, and nobody enjoys friction over every purchase. The Cash Freedom Model can lower the temperature while raising clarity: you know what you can spend and still stay on track with saving and investing. It also can steady the ride for irregular income so month-to-month swings don’t run your life.

This can work for couples, singles, those just starting out, and the ultra high net worth family with a lot of complexity.

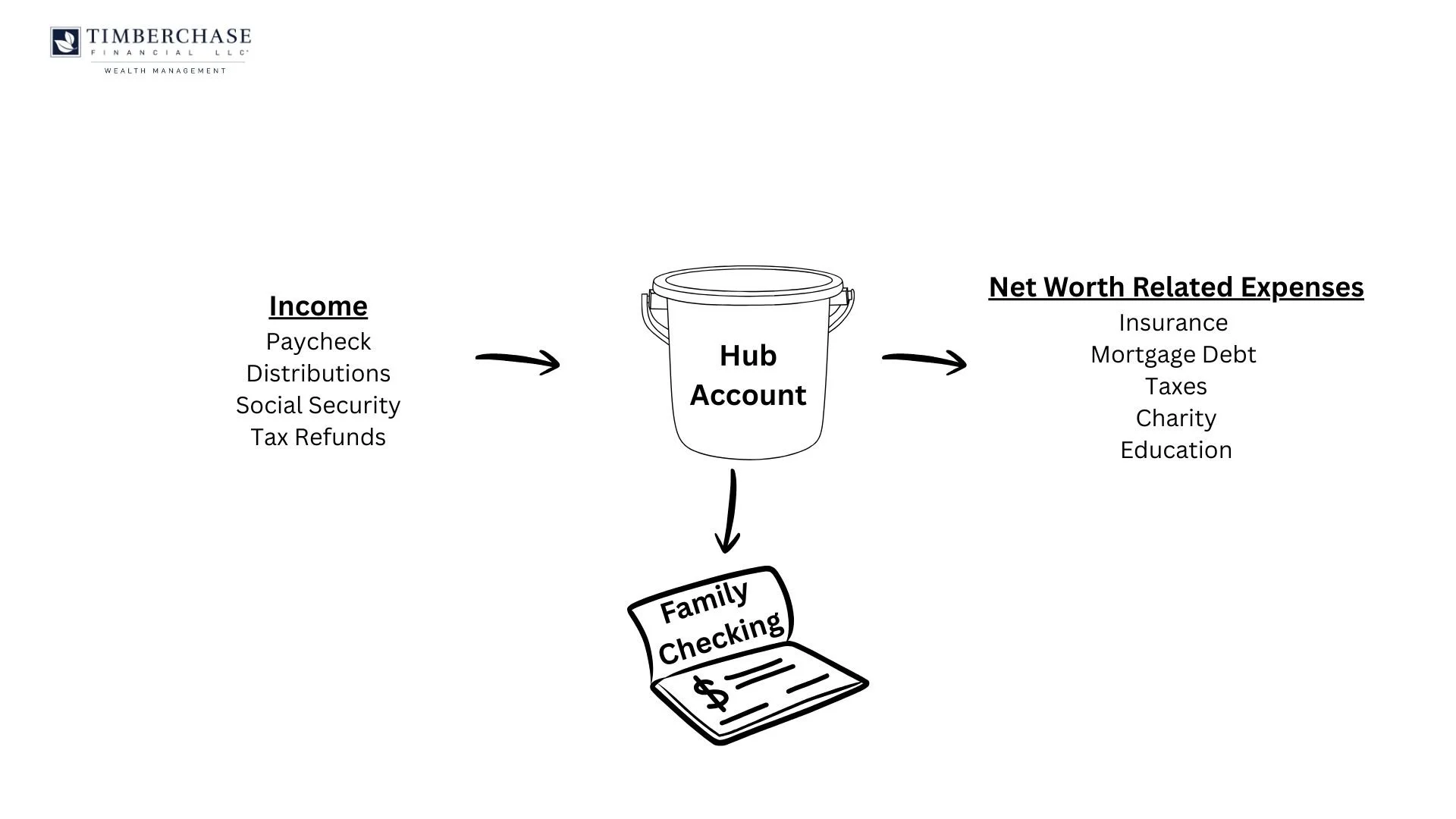

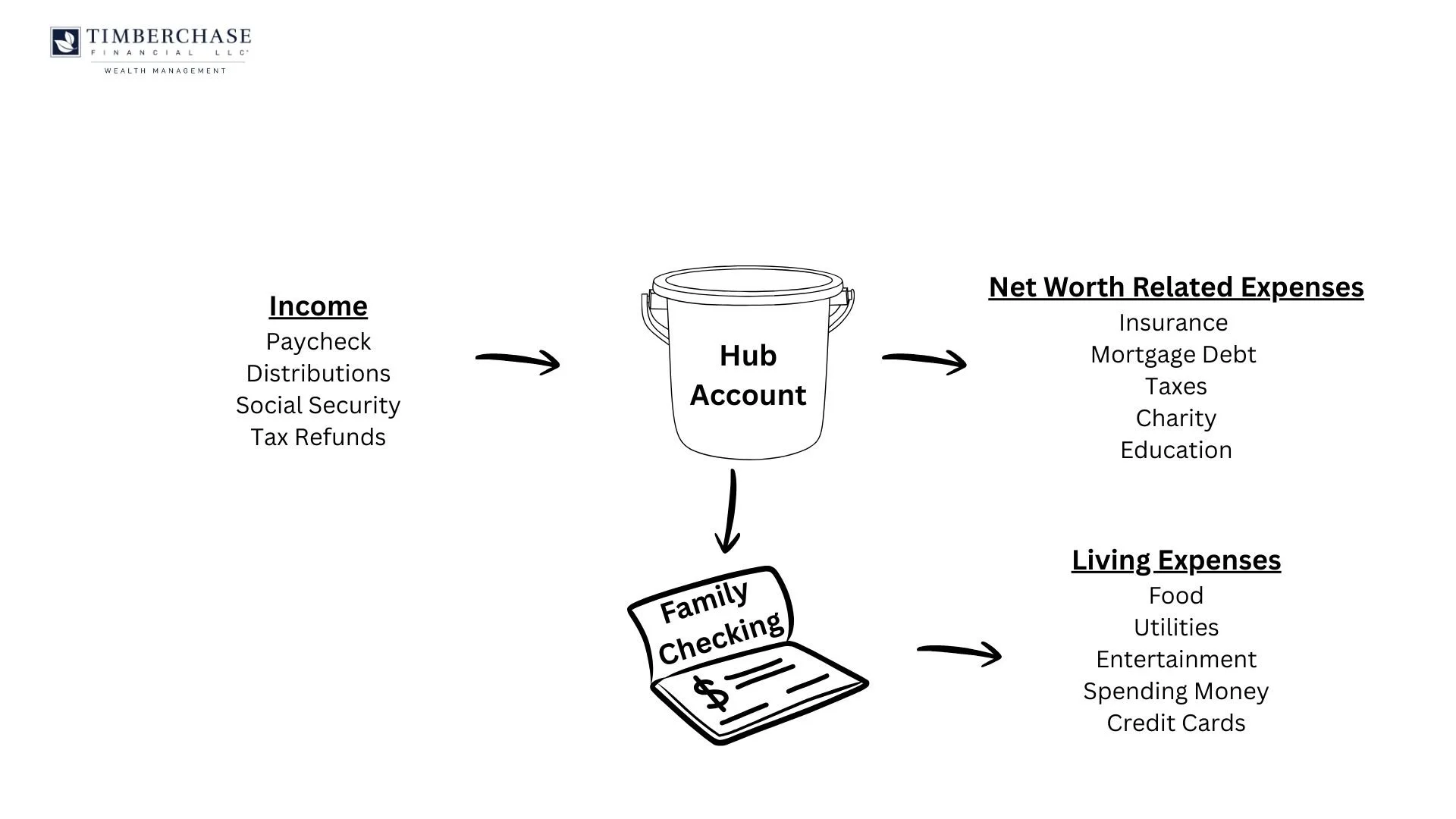

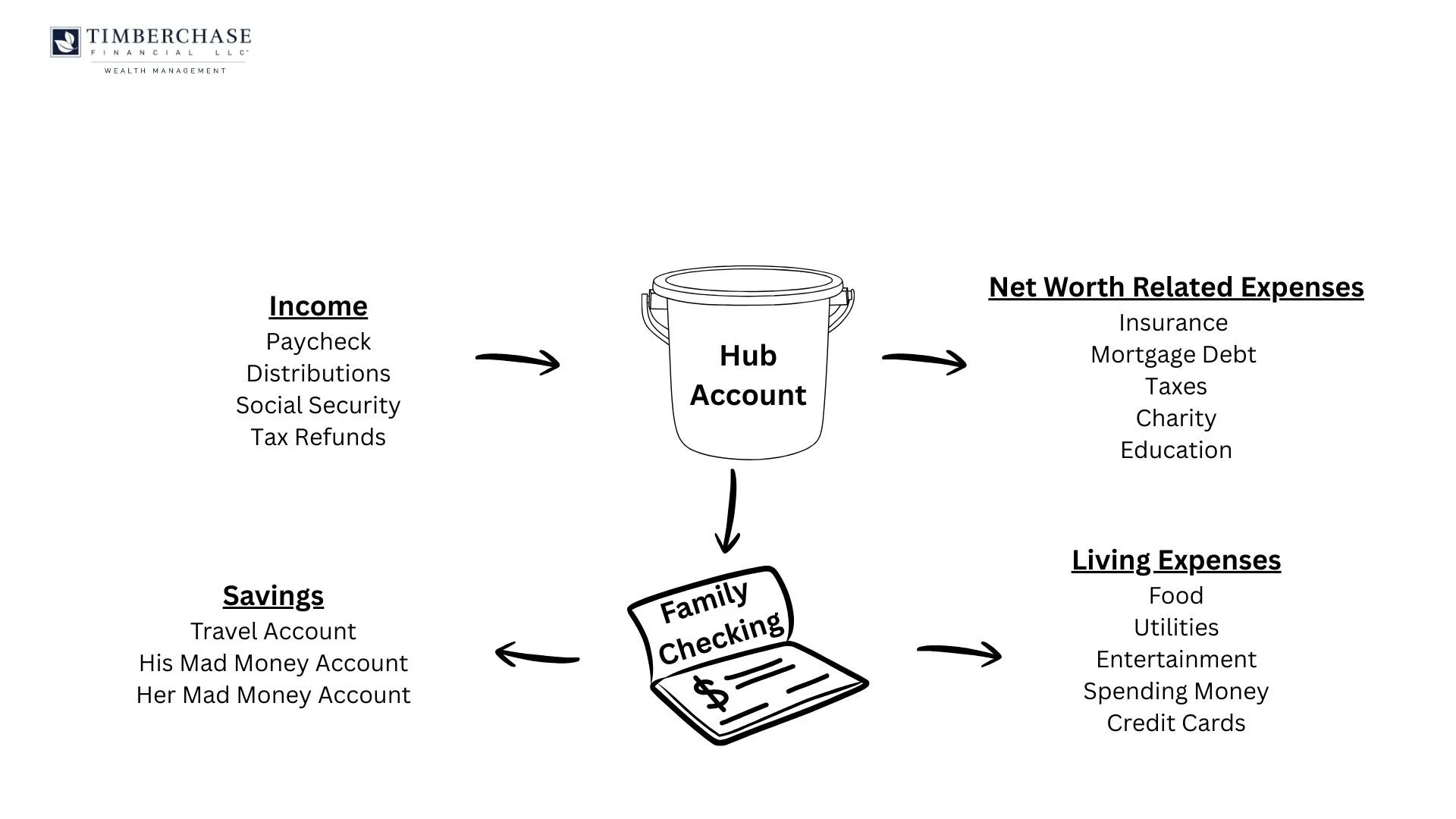

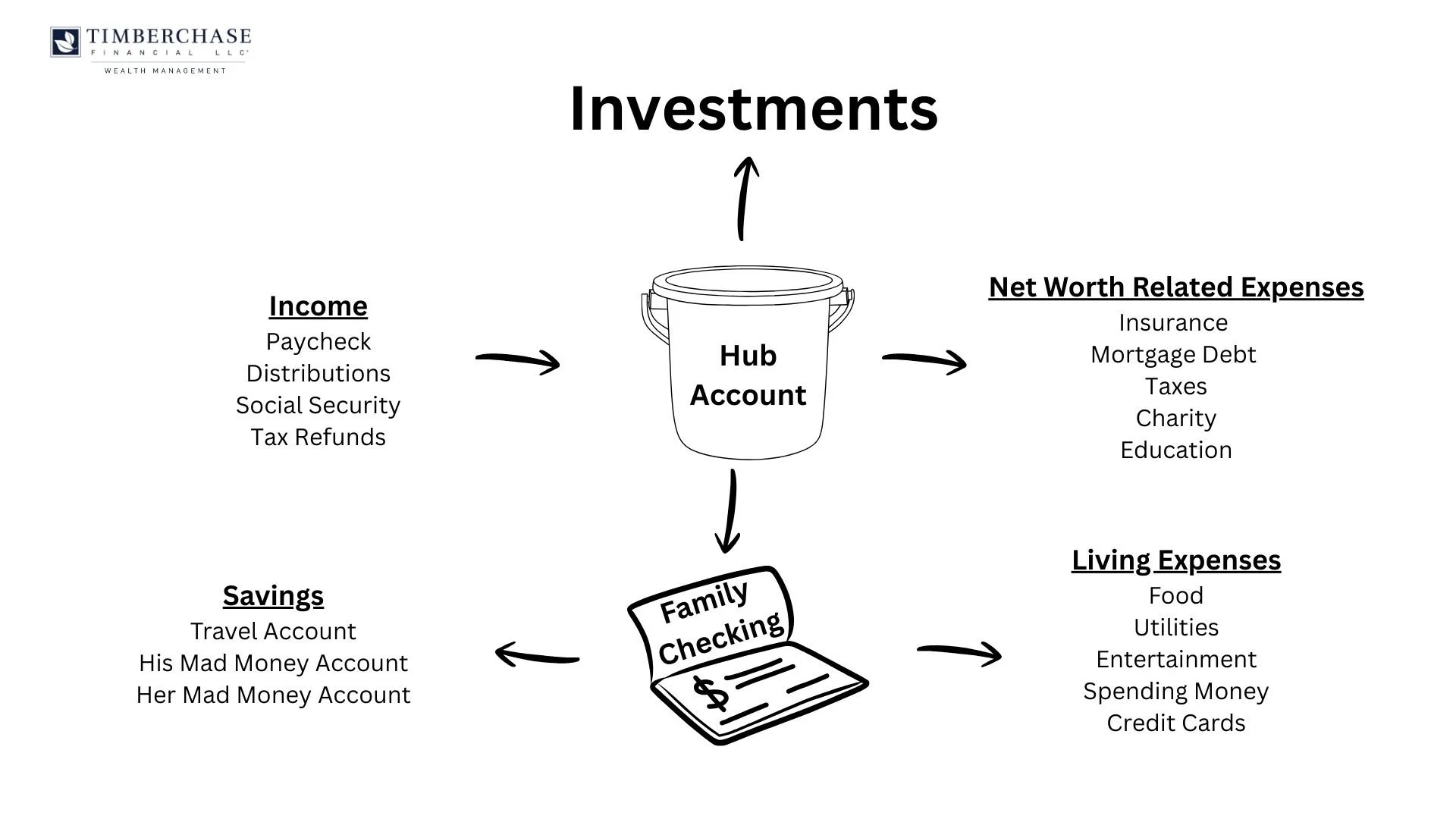

At its core, this is a two-account system and each account has a job. The Hub is where money arrives and big-picture items get handled. Family Checking is where life happens. The separation sounds simple—and it is—but that separation is what creates accountability and freedom at the same time. You get one clean monthly signal (the allowance), and you stop negotiating every purchase.

Net Worth drives lifestyle, not income

When most families live as if income pays the bills, lifestyle becomes tied to pay cycles, bonuses, and market moods. We flip that: in our view lifestyle should be set by net worth, and your net worth—via the Hub—pays the expenses. Practically, that means all income lands in the Hub, you fund investing, taxes, protection, and debt there first, and then the Hub pays your household a fixed monthly allowance into Family Checking. Income can jump around; the allowance doesn’t. The result is a steadier life with fewer “we got a raise, so let’s spend more” moments. Your lifestyle stays on a straight line, your net worth does the heavy lifting in the background, and you get accountability and freedom at the same time.

How it works (one Hub, one Checking)

All income—paychecks, bonuses, retirement distributions, business dividends, inheritance—lands in the Hub first. From there you take care of net-worth and tax items: investing (all accounts), taxes including property tax, all insurance, medical premiums & expenses, college/private school/529, HSA contributions, and debt payments (including the mortgage but not consumer debt). Those are mission-critical decisions about protection and growth; they don’t belong in the same account that buys takeout.

On the 1st of each month, the Hub sends a fixed allowance to Family Checking. That allowance is the household’s spend number for the month. Family Checking pays for groceries, gas, utilities, subscriptions, clothes, kid activities—anything that basically goes down in value when you buy it. If this account has money in it, live your life. If it’s running low, that’s your cue to ease up or explore a higher allowance that fits reality. No spreadsheets required.

Why families like it

Two words we hear often: freedom and control. Freedom, because you’re not micromanaging multiple categories. Control, because your lifestyle follows a clean monthly rhythm that matches how bills actually show up. Business owners and anyone with uneven income may especially appreciate how the Hub account absorbs variability while the allowance stays steady. Retired or working, the lifestyle flow feels the same; when paychecks stop, the pattern doesn’t have to.

This model can also reduce money meetings. Instead of debating whether an expense “fits the budget,” you look at one number. The tone of money conversations changes: fewer negotiations, more calm.

Moving to the model (a realistic timeline)

This isn’t a 30-minute flip. Give it a 30-day transition to get the plumbing right and 3–6 months for it to feel second nature as habits settle.

Step one: redirect all income to the Hub and link the Hub and Family Checking so transfers are easy both ways.

Step two: realign autopays. Net-worth/tax items get paid from the Hub; lifestyle bills stay on Family Checking. Rename the accounts in your banking app if that helps the brain switch (“HUB” or “FAMILY CHECKING” in the memo line is surprisingly effective).

Step three: Run the first month. Watch the drain/refill pattern in Family Checking and adjust the allowance after three months based on what your net worth can handle.

FAQS:

How do credit cards fit in to this model (use them, don’t let them use you)?

Points are fine—cash-flow rules first. Explore keeping one card per role for clarity:

A Lifestyle Card for groceries/dining/utilities/subscriptions, paid from Family Checking after the allowance lands.

A Hub Card for medical, insurance, tuition, and other Hub items, paid from the Hub.

Big purchases and “Mad Money”

Future big expenses—like travel—deserve a home. Keep a Mad Money account linked to Family Checking and explore a fixed transfer on the 1st (right after the allowance hits). Some couples may also keep small personal Mad Money buckets to contain the “I want this” moments and gives each person freedom inside the plan. If you prefer, larger shared goals can live as a separate Mad Money-Travel bucket so you see progress and timing at a glance.

What about the Hub balance?

The Hub can be thought of as a “runway.” Some hold three to six months of expenses there, others more or less depending on comfort and upcoming needs. There isn’t a single right number. The goal is visibility: you can see if your runway is trending up or down and make adjustments without touching your lifestyle cadence. The runway helps with future investing decisions.

Debt and the mortgage (why they live in the Hub)

Debt payoff (not consumer debt) is a net-worth decision, not a grocery-line decision. The Hub pays it so you can evaluate payoff speed based on interest rate, risk, and goals—without letting tonight’s dinner ride on it. Keeping debt in the Hub also prevents lifestyle spending from crowding out important reductions in risk when they make sense.

Common friction points (and easy fixes)

Allowance feels too tight? Explore a modest increase after evaluating how it impacts your overall plan.

Hub trending down too fast? Verify that lifestyle bills aren’t sneaking into the Hub; consider trimming a category or delaying a nonessential.

Windfalls? Bonuses, refunds, liquidity events land in the Hub. The allowance stays flat. Deployment gets planned thoughtfully. (Inheritance can be different; we cover that on our inheritance page.)

Why this outperforms budgeting (for most people)

You swap category policing for one clear monthly signal. Everyone sees the same picture. Saving and investing happen before lifestyle creep. Cash flow feels calmer—even when income doesn’t. That combination—accountability with room to live—tends to stick.

Don’t I still have to budget?

Yes—about once a year, or whenever there’s a significant life change (new job, raise, baby, move, retirement, big debt change). Spend an hour or so to revisit the allowance with fresh numbers (prices, goals, income, debt). Adjust it, re-label any bills that drifted to the wrong account, and you’re done. Spreadsheet lovers can get their fix during this annual tune-up—then close the file and go live your life for the next 12 months while the Cash Freedom Model does the day-to-day work.

Investment Decisions: How does this help

When the Hub shows a healthy, rising cash balance, that’s your cue to push dollars upstream into investments—on purpose, not by accident. The Hub gives you visibility: once the allowance and net-worth items are covered, surplus isn’t “extra spending,” it’s future growth. Where it goes next usually comes down to tax because the primary consideration on which account to invest in is how the accounts are taxed. The point is rhythm—convert excess cash into invested dollars on a regular cadence so lifestyle stays flat while net worth climbs. The Hub makes the signal obvious; you just follow it.

Want help setting this up?

Book a 15-minute Cash Freedom Review with Timberchase, and we’ll explore with you how this process might help improve your financial plan.

-

Information presented is for educational purposes only and is not personalized investment, financial, legal, tax, or accounting advice. Nothing on this website should be interpreted to state or imply that past performance is an indication of future performance. All investments involve risk and unless otherwise stated are not guaranteed. Be sure to consult with tax, legal, accounting, and financial professionals about your specific situation before implementing any planning strategies. Investment Advisory Services offered through Timberchase Financial, LLC, a Registered Investment Adviser with the U.S. Securities & Exchange Commission. Registration does not imply a certain level of skill or training.