Financial Planning in an Age of Abundance

May 8, 2026 - If you step back and look at the long arc of human living standards, you may realize the baseline lifestyle of modern life is closer to paradise compared with almost all of history. For most of human history, the average person lived very close to the edge in squalid conditions.

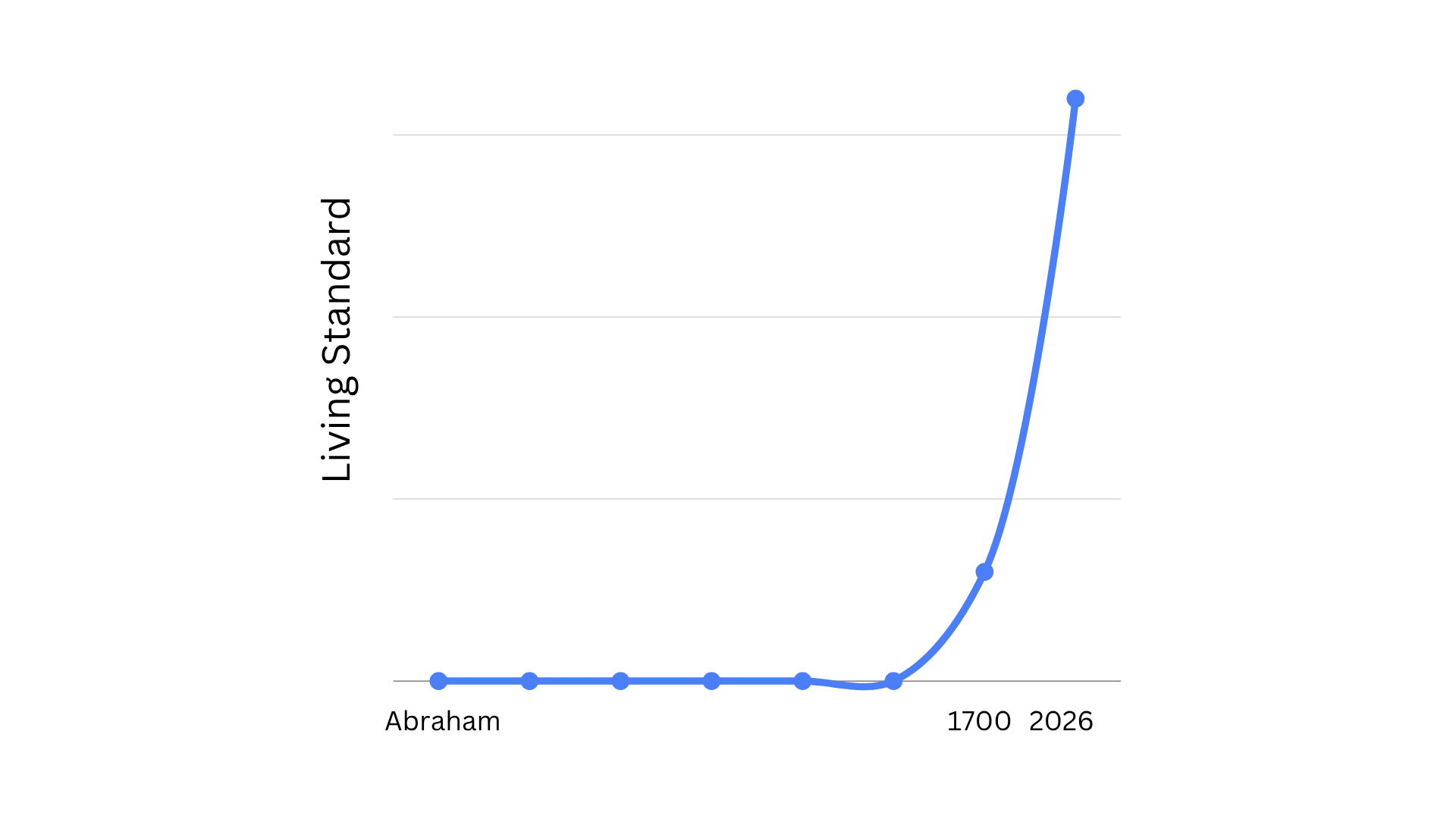

If you were to draw standard of living on a graph, starting with the time of Abraham, Isaac, and Jacob, and extend that line through the ancient world, Greece and Rome, the Middle Ages, and well into the early modern period, it would be almost flat. There were always wealthy people, but for the average person, life remained hard, fragile, and materially poor. Most people spent their days trying to get enough food, stay alive, keep their children alive, and make it through the next day.

Life Expectancy Then and Now

One way to think about living standards is to look at life expectancy. Even as late as 1800, no country had a life expectancy above 40 years, and in some places it was closer to 25. The ordinary human experience was far more vulnerable than ours is today.

When Human Living Standards Started to Change

Somewhere after 1700, and especially as you move into the late 1700s and 1800s, the line begins to rise in a noticeable way. At first, the change is gradual, then it becomes more obvious. By the late 1800s—and especially the 1900s—it starts rising much faster.

Low for a very long time. Then a bend upward. Then a much steeper climb as the modern world takes shape.

What Changed After 1700

Several things happened at the same time beginning after 1700 that changed the human experience: better agriculture, industrialization, clean water and sanitation, electricity, antibiotics, education, and changes in government structure. Then came better housing, refrigeration, transportation, communication, and safer food systems. And now, technology.

The great break in living standards is recent when you look at the full sweep of history.

Modern Life Is Not Normal

So when I draw that graph, I am trying to communicate that we are living in a historical age of lifestyle abundance. What feels ordinary to us would have looked extraordinary to almost everyone who came before us.

We expect what we have because we were born into it. We did not build most of it. We simply inherited it as the baseline condition of modern life. And in America, even the poorest among us live in relative wealth when viewed across all of history.

Economic Headlines and Financial Anxiety

There is always something to worry about: inflation, interest rates, the market, a recession warning, political change, global disruption, or a fresh prediction about what the next quarter may bring. Headlines can create the feeling that one’s financial condition is one bad development away from falling apart.

Poverty Grips People and Wealth Can Too

As most of the world before 1700 knew—and about 10% of the world population still knows today—poverty is gripping. It consumes attention, forcing a person to think about immediate needs, immediate dangers, immediate tradeoffs, and not much else. Poverty is gripping because it leaves little margin.

But in a prosperous society, wealth can be gripping as well. We can be consumed with maintaining, protecting, organizing, optimizing, tracking, and improving what we have. There may always be one more account to review, one more tax issue to think about, one more insurance question, one more market concern, one more estate planning detail, or one more urgent financial decision. In that sense, abundance can become its own form of captivity.

Poverty can grip a person by narrowing life down to survival. Wealth can grip a person by narrowing life down to management.

The Purpose of a Financial Plan

A financial plan should help us make better decisions. It should improve tax efficiency, strengthen protection, clarify retirement readiness, clean up estate planning, and bring discipline to investing. All of that matters.

But if the planning process is detached from purpose, it can become little more than organized accumulation and organized anxiety. It can become a sophisticated way to chase more and worry more.

The better use of financial planning is to put money in its proper place and help us live wisely in our abundance. It is to reduce needless anxiety, support good stewardship, and free up time and attention for what matters most. It is to help people avoid being gripped by the management of wealth. It is to help them live lives of purpose rather than lives consumed by abundance.

Financial Planning and Purpose

We have more than we realize. We fret more than we should. And if we are not careful, we can spend our lives improving our bottom line without ever asking what that improved condition is meant to do for us.

If you would like to have a conversation about the purpose behind your financial plan, please contact us.

-

Information presented is for educational purposes only and is not personalized investment, financial, legal, tax, or accounting advice. Nothing on this website should be interpreted to state or imply that past performance is an indication of future performance. All investments involve risk and unless otherwise stated are not guaranteed. Be sure to consult with tax, legal, accounting, and financial professionals about your specific situation before implementing any planning strategies. Investment Advisory Services offered through Timberchase Financial, LLC, a Registered Investment Adviser with the U.S. Securities & Exchange Commission. Registration does not imply a certain level of skill or training.